The structural shift

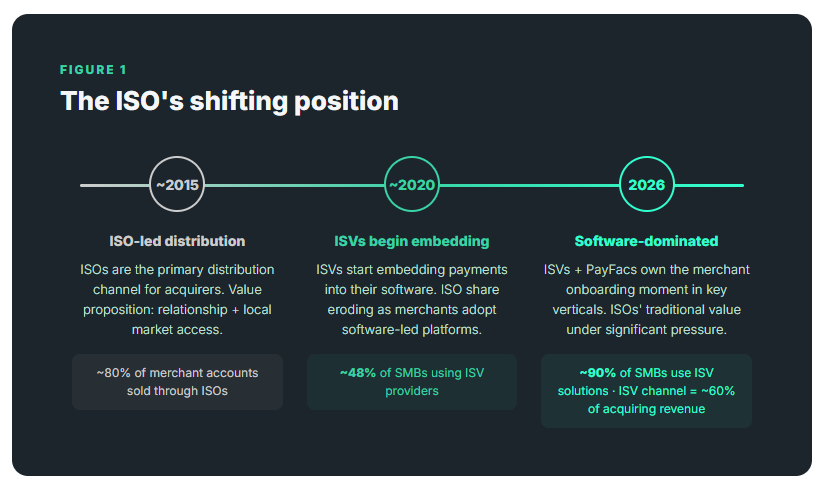

The traditional ISO (Independent Sales Organization) model was built on a straightforward value exchange: merchant acquisition in return for residual revenue on processing volume. For decades, ISOs were the primary distribution channel for acquirers — and for the acquirers who relied on them, the ISO network was the engine behind merchant portfolio growth. By some industry estimates, roughly 80% of all U.S. merchant accounts were historically sold through ISOs (Clearly Payments, 2025).

That share is now contracting rapidly. McKinsey’s January 2026 research found that approximately 90% of U.S. SMB merchants now use an ISV (Independent Software Vendor) solution for payments or business management — up from 48% just four years earlier. ISV payment-processing revenue has reached an estimated $16 billion, representing roughly 60% of the total acquiring revenue available from merchants. The ISV channel is growing at three times the rate of traditional channels (McKinsey, 2026).

The implication extends beyond ISOs alone. As software platforms absorb the merchant onboarding moment and the daily operating relationship, the ISO’s historical role — relationship-driven distribution — faces a narrowing window of relevance. And because acquirers depend on ISO networks for merchant reach, the pressure on one side of that partnership compounds on the other. Our briefing note, The merchant engagement gap, explores the acquirer’s side of this equation — why the gap between “processes payments” and “has a daily relationship” has become the most significant vulnerability in traditional acquiring. This piece focuses on the practical question: what can ISOs — and the acquirers behind them — do about it?

Why "become an ISV" doesn't align with the operational realities for most ISOs

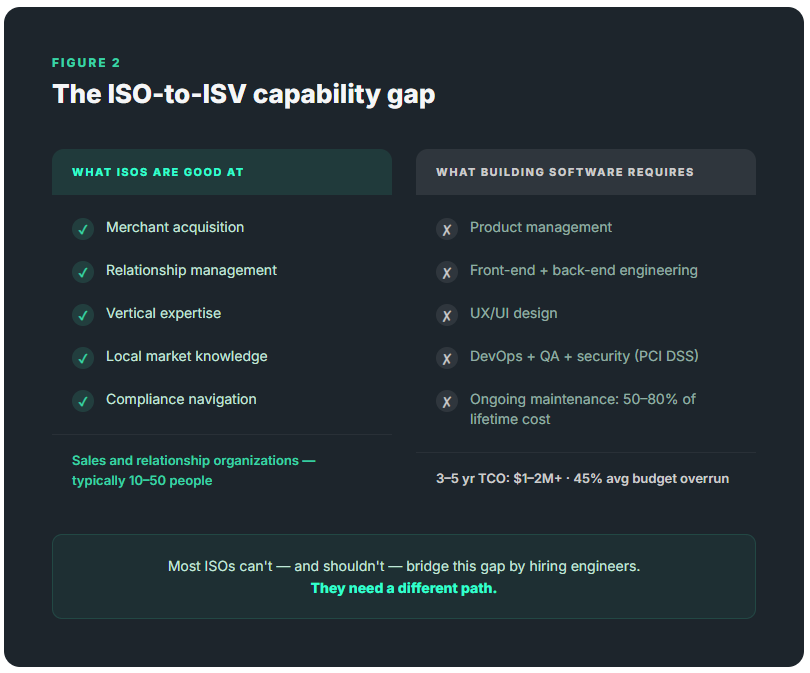

The standard industry prescription — for ISOs and for the acquirers, encouraging them to evolve — is to become a software company. It follows a reasonable logic: if software is where the value is moving, build software. But the prescription overlooks what ISOs actually are — sales and relationship organizations, typically staffed at 10–50 people, with deep vertical expertise and strong merchant networks. They are not engineering firms.

Building a competitive merchant-facing platform requires a specialist team that most ISOs would need to recruit from scratch: product management, front-end and back-end engineers, UX/UI designers, DevOps, quality assurance, and a security function capable of maintaining PCI DSS compliance year-round.

But the initial build is only the entry ticket. Research consistently shows that maintenance, updates, and ongoing compliance represent the majority of total software cost over a product’s lifetime — IBM estimates 50–75%, while Gartner puts the range at 55–80% (Idea Link, citing IBM, Standish Group, and Gartner).

The risk profile compounds the cost challenge. McKinsey and the University of Oxford, in a study of more than 5,400 IT projects, found that large software projects run 45% over budget on average while delivering 56% less value than predicted — and every additional year on the timeline increases cost overruns by a further 15% (McKinsey & Oxford, 2012). For ISOs, a software build that overruns its budget and timeline is not a strategic setback — it can be a potentially severe financial and operational consequence.

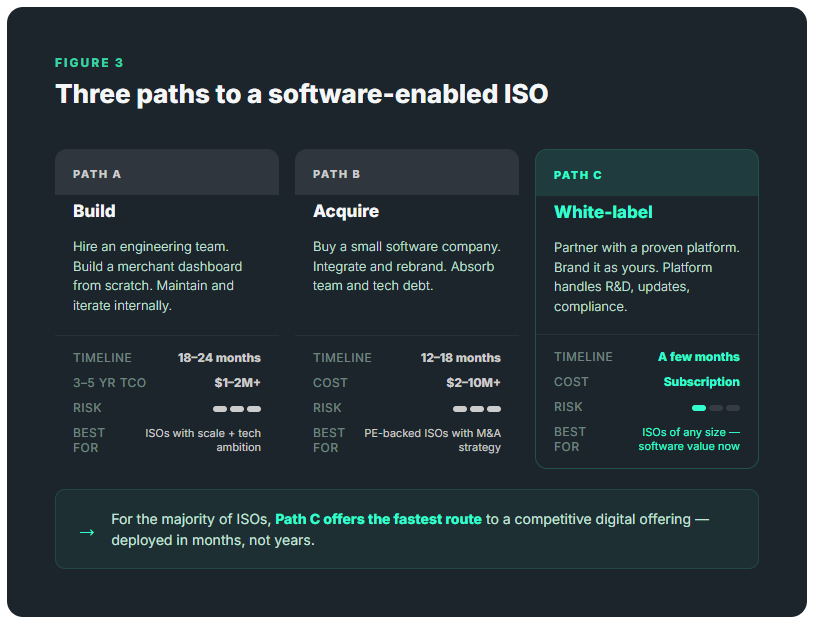

The three paths to a software-enabled ISO

ISOs don’t need to become software companies. They need a software layer on top of what they are already strong at—and acquirers need their ISO partners to have one. The strategic question is how to get there. There are three options.

Paths A and B have produced results for a small number of ISOs with the scale and capital to sustain them. In-house builds have worked where an ISO had sufficient funding to support a multi-year product roadmap and recruit a dedicated engineering function — typically at the upper end of the market, with long reinvestment horizons and a willingness to absorb the overrun risk inherent in custom software development. Acquisition-led strategies have similarly required significant capital, PE backing, and the operational capacity to integrate effectively. Both approaches demand resources, time, and risk tolerance that most ISOs do not have. Even with ISOs that can support paths A and B, the opportunity cost of these options can be significant.

For the majority, Path C — white-labelling a proven platform — offers the fastest route to a competitive digital offering. Acquirers and ISOs are already deploying white-label platforms in a few months rather than building over 12–18 months.

What the white-label model delivers

A white-label digital operating system gives an ISO the same capability set that ISVs are building with dedicated product and engineering teams — deployed under the ISO’s own brand.

The strategic logic: the strengths ISOs already have — merchant relationships, vertical expertise, local market knowledge — become significantly more defensible when wrapped in a software experience that merchants engage with daily. And for acquirers, an ISO partner with this capability is a stronger, more resilient, and defensible distribution partner.

The value shift

Software enablement does not replace what ISOs do well. It transforms the relationship's underlying economics.

Industry data illustrates the gap. High merchant attrition creates big replacement costs and lost revenue for ISOs — software enablement helps fix this with better retention and loyalty (McKinsey, 2026; TSG AIM). By contrast, ISVs that embed payments show stronger merchant retention and loyalty through daily use of their platforms (McKinsey, January 2026).

The acquirer dimension

For acquirers who depend on ISO distribution, this shift has direct implications. TSG’s 2025 directory data shows that 72% of the top 50 acquirers by volume now utilise the ISV sales channel (TSG, 2025) — and that share is growing.

When ISO partners are software-enabled, the acquirer’s distribution channel strengthens across several dimensions: lower merchant attrition, richer portfolio data, and differentiation on operational value rather than pricing. Software-enabled ISOs do not just navigate the embedded-payments transition — they become more defensible partners for the acquirers behind them.

The inverse is also true. Acquirers who equip their ISO networks with white-label digital operating systems are not simply helping their partners evolve — they are protecting their own merchant portfolios from the pressure from embedded payments models described in Part 1.

The remaining opportunity window

The ISO-to-ISV conversation is no longer theoretical. McKinsey characterizes the U.S. ISV market as having entered “Stage 3: Consolidation and maturity” (McKinsey, 2026). TSG data shows that 84% of all card-accepting merchants already use an ISV service (TSG, 2025). The volume that has not yet shifted to software-led channels is shrinking — and with it, the time available to respond.

For ISOs — and the acquirers whose distribution depends on them — the lowest-risk, shortest-time-to-value path is a white-label platform partnership. The capabilities exist. The deployment timelines are measured in a few months. The evidence indicates that merchants already seek such functionality from their payment providers.